July brought a new wave of buyer activity not typically seen in late winter, with properties starting to sell faster than they hit the market, REINZ’s latest figures reveal

Chief Executive Jen Baird says while listings continue to increase, the rise in sales volumes has seen the total number of properties for sale in New Zealand fall compared to last month. However, median prices have decreased by 2.2% nationally compared to a year ago, indicating that houses sold at a lower price in July.

The total number of properties sold in New Zealand increased by 14.5% year-on-year, from 5,070 to 5,806, and by 19.7% compared to June 2024, from 4,851 to 5,806. Thirteen regions saw an increase in sales for July 2024. The most significant increases were in Gisborne (+53.6%), Otago (+45.7%), Marlborough (+42.9%) and Southland (+38.8%). Compared to June 2024, only one region saw a decrease in sales volume, Nelson (-21.2%).

“Although we have not yet reached the spring selling season, we are observing early signs of growth in the market not typically associated with this time of year. This can be seen through the seasonally adjusted data, which indicates an increase of 5.4% in national sales compared to last year, which reflects a market performing above anticipated levels.”

Fourteen of the fifteen regions have seen a rise in new listings year-on-year, with Wellington (+55.0%), Gisborne (+50.0%) and Southland (+36.9%) leading the way. The only region to see a decrease in new listings year-on-year was Taranaki (-4.8%).

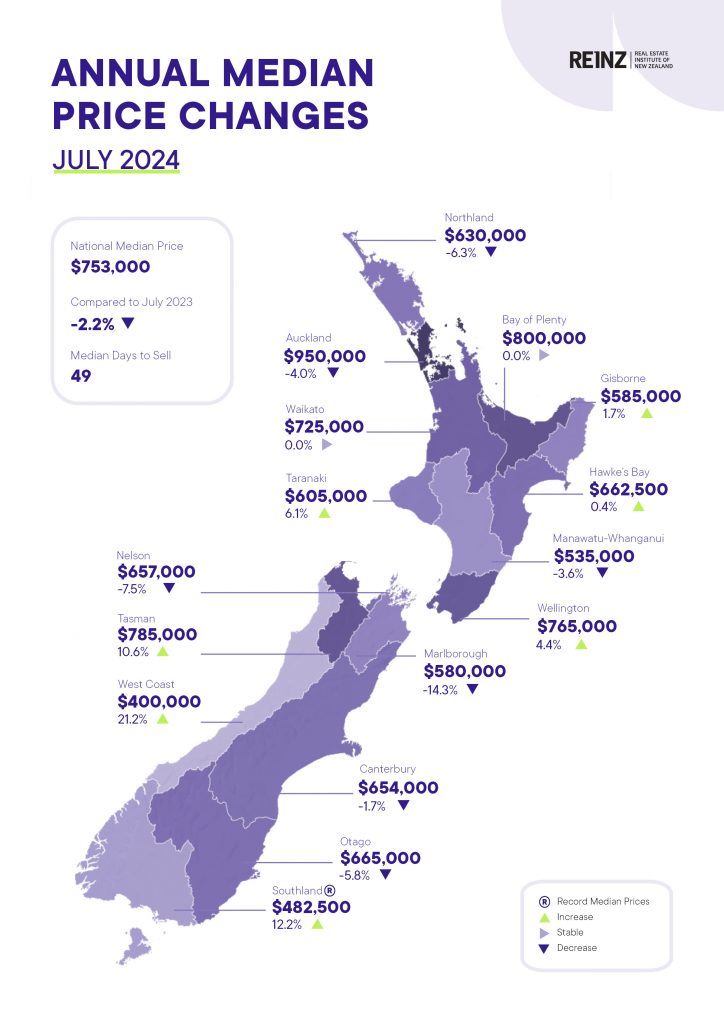

Seven of the sixteen regions had a median price increase year-on-year. West Coast and Tasman stood out, with West Coast’s median price increasing by 21.2% year-on-year ($330,000 to $400,000), and Tasman saw a 10.6% increase ($710,000 to $785,000). Seven regions saw an increase month-on-month (Waikato +3.4% to $725,000, Bay of Plenty +2.0% to $800,000, Tasman +8.7% to $785,000, Nelson +1.4% to $657,000, West Coast +25.0% to $400,000, Otago +6.4% to $665,000 and Southland +9.9% to $482,500).

The national median price decreased by 2.2% year-on-year, from $770,000 to $753,000, and decreased by the same amount month-on-month. For New Zealand, excluding Auckland, the median price decreased 1.5% year-on-year from $680,000 to $670,000. Month-on-month, the median price also decreased by 1.5%.

“There has been downward pressure on prices in most parts of the country this year and sales volumes have been lower than average as the cost of living, concerns around job security and interest rates challenge many people in New Zealand. However, it seems this sentiment is beginning to change. The slight decline in interest rates in July, and a belief that there are more to come, appears to have encouraged buyer activity, as reflected in the increase in sales,” comments Baird.

The national inventory level increased by 32.3% (+7,466) in July, from 23,090 to 30,556 year-on-year and decreased by 3.7% from 31,745 month-on-month. For New Zealand ex Auckland, inventory levels increased 30.4% (+4,409) year-on-year from 14,497 to 18,906 and decreased 3.5% (-677) compared to June 2024. There were 647 auctions nationally in July 2024 (11.1% of all sales), compared to 529 (10.4% of all sales) in July 2023. The Auckland region saw 332 properties sell by auction in July 2024 (18.4% of all sales), compared to 326 properties sold by auction or 19.1% of all sales in July 2023.

“The recent 25 basis point reduction in the OCR, and the strong signals of more reductions to come, will bring relief to households and will provide some confidence to buyers to act soon,” adds Baird.

Nationally, median Days to Sell increased by one day, from 48 to 49 days, compared to a year ago. For New Zealand, excluding Auckland, median Days to Sell had no change year-on-year (49 days). Eight regions had fewer Days to Sell in July 2024 than in July 2023. Manawatu/Whanganui had the highest median Days to Sell at 63 days, a one-day increase compared to a year ago.

The HPI for New Zealand stood at 3,563 in July 2024, a 0.2% increase from July 2023 and down by 0.3% compared to June 2024. The average annual growth in the New Zealand HPI over the past five years has been 5.2% per annum, and it is currently 16.7% below the market peak reached in 2021. Otago is the top-ranked HPI year-on-year movement this month, reaching a new peak at 4,187.

“In July, we saw an increase in sales across the country compared to last year and June 2024. As more listings hit the well-supplied market, buyers are slower to make decisions, extending the average Days to Sell. Despite ongoing economic challenges, early signs suggest potential improvement, indicating favourable conditions in the residential property landscape might be on the horizon,” adds Baird.

Median Prices

- Seven of 16 regions had year-on-year price increases with West Coast leading the way with a 21.2% increase.

- With Auckland, two of seven Territorial Authorities (TAs) had positive year-on-year median price movements with Auckland City the strongest at +13.4%, followed by North Shore District at +1.2%.

- With Wellington, seven of eight TAs had positive year-on-year median price movements with South Wairarapa District leading the way with +17.0%, followed by Kapiti Coast District at +6.9%.

- There was one regional median price record this month with Southland recording a record high median price of $482,500.

- There were two record median prices at the TA level this month. Grey District recorded a record-high price of $500,000, a 16.3% increase on the prior record set in November 2023 and Gore District recorded a record-high price of $490,000, an 11.4% increase on the prior record set in October 2023.

Sales Counts

- Nelson had its lowest sales count since January 2024.

- In terms of the month of July, July 2024 had the highest sales count in all regions (including NZ and NZ Excl. Auckland) other than Bay of Plenty, Nelson, Taranaki, Tasman and West Coast since 2021.

Median Days to Sell

- Manawatu-Whanganui had its highest median Days to Sell since February 2015.

- Taranaki had its highest median Days to Sell since February 2023.

- Hawke’s Bay had its highest median Days to Sell since June 2023.

- Southland and Waikato had their highest median Days to Sell since July 2023.

- In terms of the month of July, July 2024 had the highest median Days to Sell in:

o Marlborough since 2001

o New Zealand and Auckland since 2008

o Taranaki since 2011

o Hawke’s Bay since 2012

o Manawatu-Whanganui since 2014

House Price Index (HPI)

- Otago is the top-ranked HPI year-on-year movement this month. Southland is second and Canterbury is third.

- Otago reached a new peak HPI at 4,187

Inventory

- All 15 regions have had an increase in inventory in July 2024 compared to one year prior.

- Taranaki has had 33 consecutive months of year-on-year increases in inventory.

- Northland has had 28 consecutive months where their inventory has been at least 15% higher than the same month the year before.

Listings

- All but one region had a year-on-year increase in listings in July 2024 compared to one year prior, with Taranaki the only region not to have an increase (-4.8%).

- Auckland has had 7 consecutive months where their listings have been at least 20% higher than the same month the year before.

- Hawke’s Bay has had 7 consecutive months where their listings have been at least 15% higher than the same month the year before.

Auctions

- Nationally, there were 647 auctions in July 2024, 11.1% of all sales, compared to 529 auctions or 10.4% of all sales in July 2023.

- In Auckland there were 332 auctions in July 2024, 18.4% of all sales, compared to 326 auctions or 19.1% of all sales in July 2023.

- In Gisborne, there were 8 auctions in July 2024, 18.6% of all sales, compared to 7 auctions or 25.0% of all sales in July 2023.

- In Canterbury, there were 150 auctions in July 2024, 15.4% of all sales, compared to 108 auctions or 13.0% of all sales in July 2023