JLL New Zealand explores how commercial property is performing in the country’s three largest cities and how those markets are poised for the remainder of the year

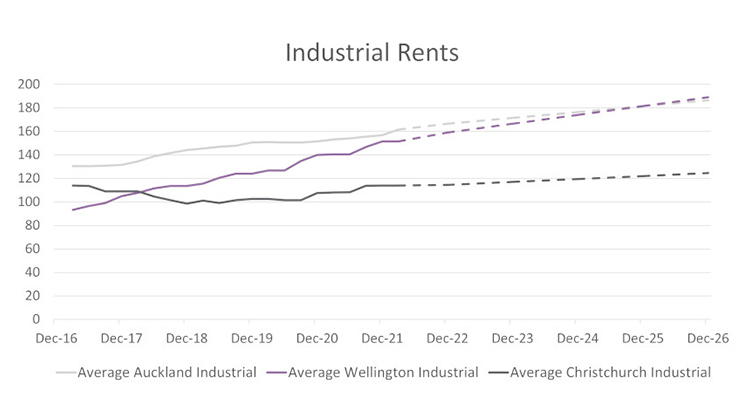

Industrial Market

The logistics and industrial property markets in Auckland, Wellington and Christchurch continue to be the most active. Low availability of stock, limited opportunities for development and unrelenting demand continue to push industrial rental rates upward.

In addition to the above, a myriad of additional factors like supply chain issues have seen vacancy maintain record low levels in Auckland’s industrial precincts. With vacancy sitting at around a mere 0.9%, tenants are competing strongly for quality space with prime yields maintaining a historical low from the previous quarter while secondary industrial yields firmed due to the competitive nature of the sector.

The current market conditions in Wellington are tight, with no signs of any relent in the pressure on the extremely low vacancy levels for the foreseeable future. While demand remains high, little is being added to supply with the pipeline bottlenecked by the continuance of rising land and constructions costs as well as the diminishing availability of industrial development land.

While both Auckland and Wellington share a similar story, Christchurch is drawing on its potential to deliver on interest from a wider pool of occupiers and investors capitalizing from a more sustainable and longer-term supply of land. Investors remain interested in Christchurch although new developers will still need to take note of required rentals to provide the appropriate returns to meet investment thresholds.

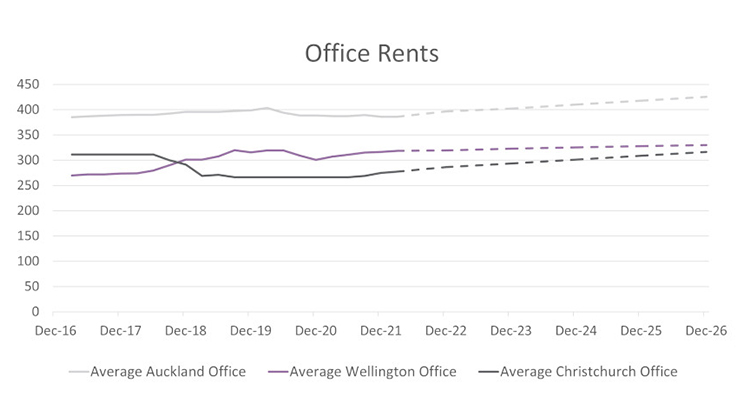

Office Market

This year has seen the continuation of workspace strategies evolving, with an increase in requirement from occupiers towards employee health and wellbeing and fulfilling green initiatives. Quality office spaces will remain a key strategy for occupiers as part of their retention and attracting of staff.

While overall vacancy has increased in the Auckland CBD, there is an uneven spread of occupancy across the city on a building-by-building basis. Meanwhile vacancy among offices on the Auckland city fringe has decreased. However, with the borders due to open there is an expectation for investment enquiry to increase along with the ‘great return to work’ which will see occupancy levels rise once more.

Vacancy rates in the Wellington office property market illustrate a unique story with prime increasing minimally to a mere 1.1%, while secondary vacancy decreased to just 4.3%. Occupation is being driven by government tenants and lack of office supply, however there are a number of office developments in the pipeline with many offering mixed use. While these are predominantly already fully pre-leased, this is expected to create a quantum of backfill space in A-grade buildings.

While there were no office completions in Christchurch for the first quarter of 2022, there are many developments in the pipeline including 28 in the central business district alone. As a consequence of the historically low vacancy levels among prime office offering, demand for secondary properties has been bolstered.

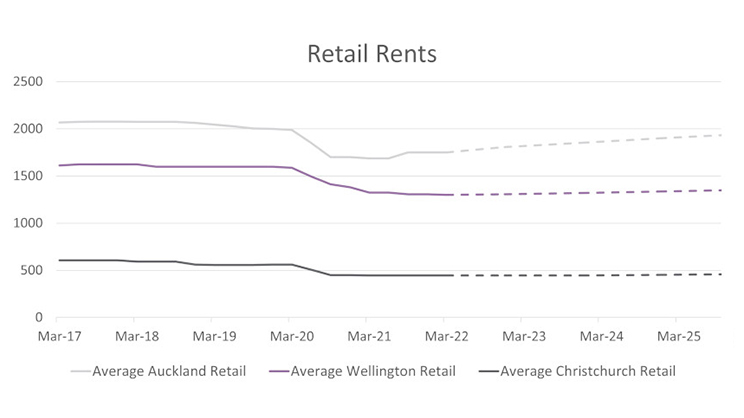

Retail Market

Even though the retail property market continues to be one of the hardest hit industries from the pandemic due to enforced lockdowns and trading restrictions, increased leasing momentum indicates a positive direction since the pandemic made its presence known. While there are few sole retail developments in the pipeline in New Zealand, retail is a key component of several mixed-use developments comprising office, hotel or apartments.

Overall vacancy among retail real estate in the Auckland CBD decreased during the quarter, showing uptake of vacant opportunities as come to the market. The future of Auckland CBD retail will be supported by employees returning to the office, students to university and tourism. Demand has maintained for suburban retail with many consumers opting to shop locally while working from home.

Wellington’s “Golden Mile” extending from the Parliament end of Lambton Quay, along Willis St and through to Manners St to the eastern end and entertainment hub of Courtenay Place is expect to gain back its momentum after being hit hard by the reduced footfall. Average gross rents have held steady as have yields.

The outlook for retail real estate in Christchurch remains positive with continued low vacancy in both suburban and CBD precincts. With borders due to open and workers returning to the workplace, the CBD is set to benefit from an influx of footfall, while it is expected that suburban retail will continue to benefit from the ‘shop local’ philosophy for those that have adopted hybrid or remote working structures.